Higher US interest rates test the world

August 2022

New York’s Plaza Hotel, in financial circles, is best known for when the finance ministers of France, Japan, the UK, the US and West Germany gathered in 1985 to suspend the free-float of the US dollar.

The problem the ministers sought to solve was the US dollar had soared 44% since 1980 because US interest rates had jumped over that time. The world was worried that the subsequent widening of the US trade deficit could prompt Washington to restrict imports. Under the Plaza Accord, the G-5 agreed to lower the US dollar over the following two years. The intervention, which drove down the US currency by 40%, is still the biggest manipulation of the US currency since it was floated in 1973.[1]

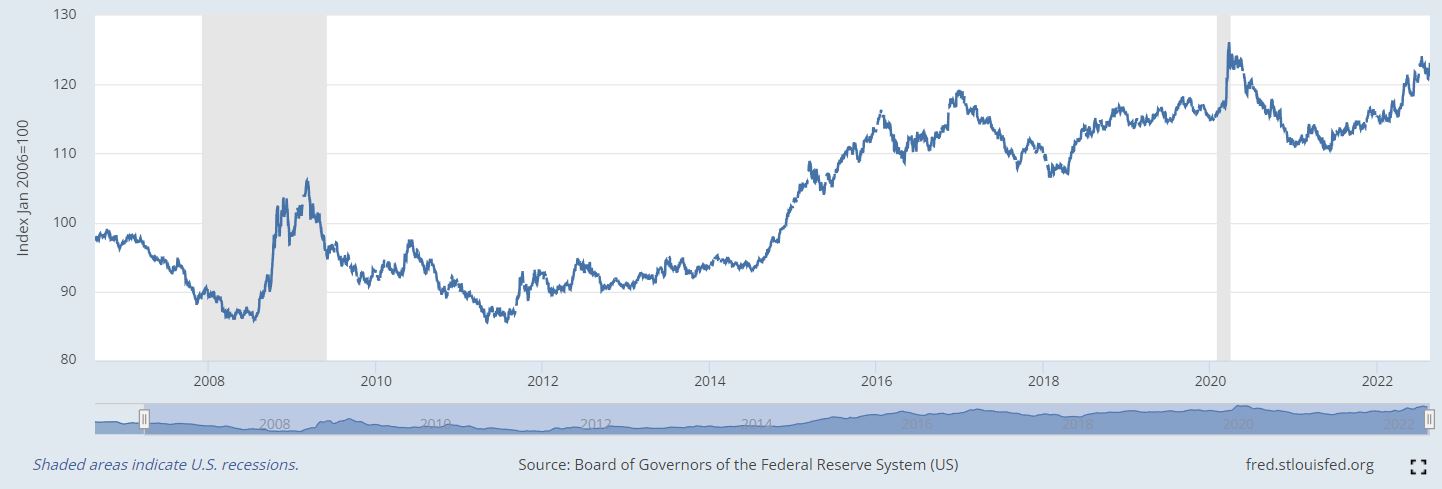

Another Plaza Accord might be needed in coming times.[2] Once again, rising US interest rates are boosting the US dollar to heights that trouble the world. Against the ‘real broad dollar index’, the US currency has surged 10% over the past year to its highest since this index was compiled in 2006.[3] The US dollar is likely to stay strong because the Federal Reserve needs to smother inflation that reached a 41-year high of 9.1% in the 12 months to June. The Fed raised its benchmark rate from about 0% in March to between 2.25% and 2.5% in July and more rate increases are almost certain.

Higher interest rates in the world’s largest economy always present challenges for the world. Today’s trials wrought by higher US rates, however, could be more troubling than usual because the pandemic and Russia’s invasion of Ukraine are magnifying the standard threats posed by higher US interest rates while minimising the usual benefits. Three difficulties stand out, starting with the higher greenback.

A stronger US dollar comes with advantages and disadvantages. Among pluses, a rising US currency eases US inflationary pressures via cheaper imports. The flip side, however, is the rest of the world confronts an inflationary shock in three ways. First, US exports cost more in other currencies. Second, trade priced in US dollars between non-US parties becomes more expensive in other currencies. An IMF paper in 2020 estimated about 40% of global invoices are priced in US currency and that countries doing so “tend to experience greater US dollar exchange pass through to their import prices”.[4] The third inflation threat is that today’s strong US dollar is unusually coinciding with higher oil prices due to the Ukraine war, which magnifies the increase in oil prices in other currencies. In the past, high oil prices have usually coincided with a feeble US dollar.[5]

To counterattack the inflationary threat of a high US dollar, central banks from Canada to Singapore to Saudi Arabia to Switzerland are unexpectedly boosting key rates in bigger steps[6] to support their currencies in what has been dubbed a ‘reverse currency war’. The term ‘currency war’ was coined in 2010 to describe how central banks were lowering currencies to help exports. The futility is that all countries can’t push their currencies in the same direction at the same time.[7]

The eurozone is especially vulnerable to US-dollar-imported inflation, even allowing for an export boost to the US. The euro in July fell to a 20-year low (below parity) against the US dollar, to mark a 14% drop since January 1. Higher import prices, pandemic disruptions to supply and higher food, energy and commodity prices stemming from the Ukraine war propelled eurozone inflation to a record 8.6% in the year to June. In response, the European Central Bank in July raised its key rate by 50 basis points to 0%, to end eight years of negative rates.

While the ECB’s delay in raising rates has undermined the euro, the lag and tumbling currency are more because the eurozone’s economic fundamentals are so weak.[8] The ECB is worried that inflation will drive yields on the sovereign debt of indebted euro members to levels that trigger another financial crisis and possible exits from the common currency.

A second challenge of higher US rates is they hamper the US economy. US GDP, which is about 70% consumer spending, contracted over the first six months of 2022.[9] The immediate outlook seems problematic because the fiscal stimulus tied to the pandemic and supply disruptions have boosted inflation to levels that trouble consumers. US consumer confidence in June fell to a record low as surveyed by the University of Michigan, which has tracked US consumer sentiment since 1952.[10] A weak US economy means the high US dollar is not offering its usual boost to world exports – as it did in the first half of the 1980s.

The third challenge of higher US interest rates is they bludgeon emerging countries, especially those that have borrowed in US currency or have currencies linked to the greenback. As at May 31, the IMF said eight poorer nations were in “debt distress” and another 30 countries were at “high risk”.[11] Since then, Bangladesh, Ghana,[12] Pakistan and defaulting Sri Lanka have asked the IMF for aid. Many are concerned another 1997-style Asia crisis is festering in South Asia.[13] Indebted economies have been weakened by the pandemic and face a cost-of-living crisis resulting from the Ukraine war. The fact that emerging countries are overwhelmingly borrowing in local currencies is failing to insulate them from higher US interest rates and a stronger US dollar. A Bank of International Settlements paper in July warns how the currency risk has only shifted to creditors who invest on a US-dollar basis.[14] Thus, capital is still fleeing emerging countries.

The Institute of International Finance estimates international investors yanked US$38 billion from emerging markets in the five months to July. Outflows each month from February to July mark the longest periods of consecutive monthly net outflows since records began in 2005.[15] Emerging-country currencies tumbled accordingly – many by more than 20%. The linked inflation threat has forced central banks to raise rates to support currencies at a time when the IMF is warning that the pandemic and Ukraine war have widened current-account balances enough to trigger populist protectionist measures.[16] Concerns are rising that economic turmoil could lead to political instability. “Food and fuel inflation threatens to rip poor societies apart,” warns Murtaza Syed, acting governor of the Central Bank of Pakistan.[17]

Central banks are far from winning their battles against inflation.[18] The accelerated loop triggered by a pandemic-and-war-distorted world whereby higher US rates force other countries to raise rates could run for a while yet. The best hope for the world is that something – ideally, a decline in US inflation, but even a US recession – dampens US interest rates and averts financial upheavals in the eurozone and emerging countries.

To be sure, US interest rates are still historically low and the US dollar is well below its 1985 peak. But that matters less when government, corporate and personal debt are so high. US inflation might have already peaked – US inflation eased to 8.5% in the year to July – and the Fed might slow rate increases. But the crest of inflation could matter less than the stubbornness of inflation. If US inflation only slows gradually, US interest rates will stay elevated.

The pity is that in a world of floating exchange rates central banks outside the US, for all their domestic political independence, are tied to a Fed that misjudged inflation.[19] There’s no solution, let alone an international accord, shaping to alleviate the dangers.

The unsolvable handicap

Economists Barry Eichengreen of the US, Ricardo Hausmann of Venezuela and Ugo Panizza of Italy chose ’The pain of original sin’ as the title of their 2003 study of emerging countries. They presumably judged this Christian concept best describes an insurmountable inherent flaw.[20]

The study was a landmark because it was the first to focus on the importance of the currency denomination of foreign debt for emerging countries. The trio found the health of emerging economies depended much more on the currency breakdown of foreign debt than other aspects of macroeconomic stability such as the soundness of monetary and fiscal policies and human and physical capital accumulation. They found the foreign-currency makeup of foreign debt governed “the stability of output, the volatility of capital flows, the management of exchange rates and the level of country credit ratings”.[21]

The trouble is emerging countries need to borrow to develop. But they are generally unable to borrow in their local currency, the inherent weakness they can’t overcome.[22] The trio’s paper was written when only 2.7% of emerging debt was sold in local currency.[23]

It’s widely acknowledged that emerging countries that borrow in foreign currency are vulnerable if their currencies plunge. To reduce this weakness, bodies such as the IMF and the World Bank have long encouraged emerging countries to borrow in local currency. And they have. Over the past decade, more than 80% of the increase in emerging-country debt was in local currency – the ratio topped 95% from the end of 2019 to 30 September 2021.[24]

This is why the BIS paper on the failure of local borrowings to insulate emerging countries from currency risk is so sobering. The BIS finding means the tendency of troubles in one emerging market to infect others is as primed to detonate as always.

Average gross government debt in emerging markets stood at an estimated 64% of GDP at the end of 2021, according to the IMF. The pandemic drove a 10-percentage-point jump in that ratio.[25] Companies in emerging countries are estimated to have borrowed about 14% of global GDP.[26]

Emerging countries are the hardest hit by the blows to living standards from the Ukraine war. They are vulnerable to a Fed boosting US interest rates and a rising US dollar. Calls for a new Plaza Accord are bound to intensify.

By Michael Collins, Investment Specialist

Nominal broad US dollar index since 2006

[1] Jeffrey Frankel. National Bureau of Economic Research. ‘The Plaza Accord, 30 years later.’ NBER working paper series. Working paper 21813. December 2015. nber.org/system/files/working_papers/w21813/w21813.pdf

[2] See ‘Surging dollar stirs markets buzz of a 1980s-style Plaza Accord.’ 18 May 2022. bloomberg.com/news/articles/2022-05-18/surging-dollar-stirs-markets-buzz-of-a-1980s-style-plaza-accord

[3] Federal Reserve. Foreign exchange rates – H.10. ‘Real broad dollar index – monthly index.’ federalreserve.gov/releases/h10/summary/jrxwtfbc_nm.htm. Currencies such as India’s rupee are at record lows against the greenback while others such as the euro are close to record lows.

[4] IMF. ‘Patterns in invoicing currency in global trade.’ Emine Boz et al. IMF working paper WP/20/126. July 2020. Page 2 and 13. imf.org/en/Publications/WP/Issues/2020/07/17/Patterns-in-Invoicing-Currency-in-Global-Trade-49574

[5] See Javier Blas. ‘In the oil market, the strong dollar is the world’s problem.’ Bloomberg News. 8 June 2022. bloomberg.com/opinion/articles/2022-06-08/record-oil-prices-in-europe-asia-strong-dollar-is-becoming-the-world-s-problem

[6] See ‘Central banks embrace big rises to bolster currencies and fight inflation.’ Financial Times. 17 July 2022.

[7] See Jeffrey Frankel. ‘Get ready for reverse currency wars.’ Project Syndicate. 25 May 2022. project-syndicate.org/commentary/strong-dollar-high-inflation-reverse-currency-wars-by-jeffrey-frankel-2022-05

[8] See Paul Krugman. ‘Wonking out: The meaning of the plunging euro.’ 15 July 2022. Krugman here explains how the eurozone’s weak fundamentals correspond to the analysis of exchanges rates in German economist Rudiger Dornbush’s classic paper of 1976, ‘Expectations and exchange rate dynamics’. nytimes.com/2022/07/15/opinion/euro-dollar-fed-ecb.html

[9] The US economy shrank at an annualised rate of 1.6% in the first quarter and 0.9% in the second.

[10] University of Michigan. ‘Surveys of consumers.’ June final results. 24 June 2022. The index fell to a record low of 50.0 in June 2022 compared with 85.5 a year earlier. In July, the index rose to 51.1, a result described as “relatively unchanged, remaining near all-time lows”. data.sca.isr.umich.edu/

[11] IMF. ‘List of LIC DSAs for PRGT-eligible countries.’ 31 May 2022. LIC stands for low-income countries. DSA stands for debt sustainable analysis. PRGT stands for poverty reduction and growth trust. imf.org/external/Pubs/ft/dsa/DSAlist.pdf

[12] See ‘How Ghana makes a success out of failure.’ The Economist. 5 August 2022. economist.com/middle-east-and-africa/2022/08/05/how-ghana-makes-a-success-out-of-failure

[13] See ‘South Asia debt woes evoke fears of another 1997-style crisis.’ 4 August 2022. bloomberg.com/news/articles/2022-08-03/india-sri-lanka-pakistan-debt-woes-evoke-memories-of-1997

[14] “Exchange-rate fluctuations induce shifts in portfolio holdings of global investors, even in the absence of currency mismatches on the part of the borrowers,” the paper says. Boris Hofmann et al. ‘Risk capacity, portfolio choice and exchange rates.’ BIS working papers. No. 1031. Bank of International Settlements. 15 July 2022. bis.org/publ/work1031.htm

[15] Financial Times. ‘Emerging markets hit by record streak of withdrawals by foreign investors.’ 31 July 2022. ft.com/content/35969b19-86db-4197-a419-b4a761094e9a

[16] IMFBlog. ‘Global current account balances widen amid war and pandemic.’ 4 August 2022. blogs.imf.org/2022/08/04/global-current-account-balances-widen-amid-war-and-pandemic/

[17] Murtaza Syed, acting governor of the Central Bank of Pakistan. ‘Now is not the time to neglect developing economies.’ 3 August 2022. https://www.ft.com/content/f0e2df4c-f64b-4820-b3b3-27389b256ecf

[18]IMFBlog. ‘Soaring inflation puts central banks on a difficult journey.’ 1 August 2022. blogs.imf.org/2022/08/01/soaring-inflation-puts-central-banks-on-a-difficult-journey/

[19] Financial Times. ‘The Fed’s rate increases are a matter of high interest for everyone.’ 28 July 2022. ft.com/content/db77664b-084a-462e-8dc1-1b127fac1b35

[20] Barry Eichengreen, Ricardo Hausmann and Ugo Panizza. ‘The pain of original sin.’ August 2003. Berkeley. eml.berkeley.edu/~eichengr/research/ospainaug21-03.pdf

[21] “That the external debts of emerging markets are disproportionately denominated in foreign currency goes a long way towards explaining why their economies are more volatile and crisis prone than those of their advanced-country counterparts,” the trio conclude. Barry Eichengreen, Ricardo Hausmann and Ugo Panizza. Op cit.

[22] Stephen Mihm, professor of history at the University of Georgia. ‘Strong dollar always clobbers developing nations.’ Bloomberg News. 27 July 2022. bloomberg.com/opinion/articles/2022-07-27/strong-dollar-always-clobbers-developing-nations

[23] BIS. Op cit. Table 1. Page 28.

[24] Reuters. ‘Emerging markets drive global debt to record $303 trillion – IIF’. 24 February 2022. reuters.com/markets/europe/emerging-markets-drive-global-debt-record-303-trillion-iif-2022-02-23/. ‘Total global debt dips, but emerging market debt hits record high.’ 18 November 2021. reuters.com/business/total-global-debt-dips-emerging-market-debt-hits-record-high-2021-11-17/. The article quotes data from the Institute of International Finance.

[25] IMFBlog. ‘Emerging economies must prepare for Fed policy tightening.’ 10 January 2022. blogs.imf.org/2022/01/10/emerging-economies-must-prepare-for-fed-policy-tightening/

[26] Lorenzo Forni and Philip Turner. ‘Global liquidity and dollar debts of emerging market corporates.’ Vox EU. 15 January 2021. voxeu.org/article/global-liquidity-and-dollar-debts-emerging-market-corporates

Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 (‘Magellan’) and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.