Japan has trailblazed on economic stimulus, to not much avail

December 2020

In 2006, 52-year-old Shinzō Abe of the almost-always-in-power Liberal Democratic Party became Japan’s youngest-ever prime minister. In 2007, however, the son of a foreign minister and the grandson and grand-nephew of prime ministers resigned due to ill health.[1]

Abe recovered soon enough. In 2012, the princeling retook the leadership of then-in-opposition LDP and after elections in December that year again became prime minister of the world’s third-largest economy. On August 28 this year, Abe, now Japan’s longest-serving prime minister, unexpectedly resigned, again due to poor health.

Abe’s health-interrupted prime ministership and his deflated exit almost symbolises the fragility of Japan’s deflation-prone stop-start indebted economy since an asset bubble burst in the early 1990s. Abe’s three-pronged ‘reflationist’ revival plan launched in 2013 can be regarded as an aggressive, but largely forlorn, attempt to pull Japan out of its stagnation and ‘debt trap’ (when more debt is needed to overcome the problems left by past debt).

Abe’s ‘three arrows’ of radical monetary stimulus, diminishing fiscal prodding and microeconomic reforms were inspired by the reflation policies of his predecessor Korekiyo Takahashi (1854-1936), who “brilliantly rescued Japan from the Great Depression” in the assessment of former Federal Reserve chairman Ben Bernanke.[2] Abe’s handicap was that orthodox monetary and fiscal stimulus was largely spent when he primed his arrows to revive a deflation-riddled country with an ageing and shrinking population that leads to a chronic lack of domestic demand. By the time Abenomics was launched, interest rates were already at zero and fiscal deficits had driven Tokyo’s debt to about 230% of GDP.[3]

The Bank of Japan’s ‘bazooka’ of monetary stimulus that formed one prong of Abenomics included a buying spree of government bonds, purchases of equity funds, negative interest rates and the simultaneous targeting of the cash rate and the 10-year government bond yield. The prong of micro reforms included pushes to attract more elderly, females and foreigners into the workforce and increasing the country’s birth rate. The other prong of fiscal stimulus provided diminishing support because Tokyo reduced its deficit from 8% of output in 2012 to about 3% of GDP by 2017 to arrest the rise in government debt ratios – perhaps Abe’s greatest achievement before the coronavirus struck.[4]

But higher taxes led to sporadic contractions in the economy (while the pandemic triggered another slump and renewed deflation).[5] From 2013 to 2019, Japan’s annual economic growth averaged only 1.1% and annual inflation reached only 0.9%, while gross government debt climbed to 238% of output.[6] Stimulus this year worth 40% of GDP to fight the coronavirus will take the debt ratio much higher. The micro reforms did little for relative productivity growth – Japan’s largely improved only in line with the OECD average.[7]

Abe’s policies were drastic in parts but not drastic enough it would seem. They lacked the punch of Takahashi’s reflation efforts that enabled Japan to be the first major power to escape the 1930s depression. Takahashi’s formula was to take Japan off the gold standard to allow the yen to plunge, to slash interest rates and to use the central bank to finance government deficit spending (as in printing money Zimbabwe-style).

And therein lies one of three broad policy options for Japan under 71-year-old Prime Minister Yoshihide Suga who in September became the country’s 99th prime minister. Many observers have long speculated that indebted Japan would be the first modern major economy to print money in the quantities needed to escape stagnation and deflation. Government action to create money and hand it to the public is a recipe for growth though at the risk of inflation because more money is chasing the same amount of goods and services.

Another option for Suga would be to intensify and broaden the Bank of Japan’s asset buying to include more privately owned assets such as shares, while adding to the 50% of government bonds it already owns.[8] But quantitative easing seems better at avoiding crises than reviving economies. It would perhaps be almost akin to Suga’s third option, to do not much more at the macro level and focus on micro reforms, which, due to political challenges, tend to be longer-term minor remedies. The risk with these last two options is that Japan’s economy in coming years will only muddle through and thus could be poorly placed to deal with future shocks. The option Suga chooses, especially if he opts for money printing, will be of much interest because Japan’s path will hold lessons for other pandemic-hit economies beset with low growth and high debt.

The encouraging news about a vaccine could reduce Japan’s pertinence for other economies. Japan is a socially and politically cohesive country with a current-account-surplus. The Japanese enjoy a high standard of living and full employment and, along with Japanese firms, save their earnings. So what might work in the country might not necessarily succeed elsewhere. Nothing Suga has said suggests he will soon resort to the money printing that risks out-of-control inflation or that he will pursue more aggressive quantitative easing; he’s talked more about micro reforms.[9]

But Japanese policymakers know they need to do more to achieve sustainable economic growth. They have proven a daring lot. They could well spearhead a policy leap that will lead countries with ‘Japanification’ symptoms into a healthier economic future.

Sony led

In 1955, Canadian businessman Albert Cohen, in Tokyo to scout for opportunities, saw a newspaper advertisement that sought a distributor for a new type of radio called a transistor that had been developed by Tokyo Tsushin Kogyo. After a handshake agreement, Cohen lugged back to Winnipeg 50 radios that bore a brand name the radio maker, wanting a one-syllable word like Ford, liking the Latin word for sound, sonus, and recalling GIs post-war throwing Japanese kids chewing gum and calling out ‘there you go, sonny’, settled on as Sony. The brand’s big overseas break came in 1957 when the media reported that thieves had broken into a New York warehouse full of electronic equipment and had stolen only the 400 cartons holding tiny Sony radios.[10]

From these starts, Sony led the creation of the consumer electronics industry that helped make Japan the world’s dominant economy in the 1980s such that at the end of 1989 Japanese stocks accounted for 41% of the MSCI World Index compared with 8% at the end of November.[11] But even though the surge in Japanese stock prices, property values and the yen was based on the country’s huge current-account surpluses, it proved a bubble that burst from the early 1990s.

When Tokyo’s Nikkei Stock 225 Average peaked at the end of 1989, Japan’s gross government debt was 67% of GDP (while net debt was 23% of output) and the country’s population stood at 123 million. Authorities attempted to revive the economy with fiscal stimulus and rate cuts but had little success – mainly because authorities failed to recapitalise and reform the country’s banking system. In 1999, when the Bank of Japan reduced its key rate to zero, Tokyo’s fiscal deficits had more than doubled gross debt to 131% of GDP. In 2001, when the Bank of Japan invented quantitative easing, Tokyo’s stimulus had sent government debt to 147% of output. When Abe first became prime minister in 2006, Tokyo’s gross debt had reached 176% of GDP. Six years later when Abe resumed leadership (not long after the Fukushima Daiichi nuclear explosion and associated tsunami of 2011), the ratio had climbed to 229% of GDP (while Tokyo’s net debt was 147% of output).[12]

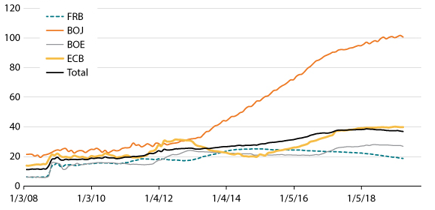

Abe never really had a fiscal arrow to fire because policymakers were wary of allowing Tokyo’s debt ratios to climb much higher. Nor was there vast room for manoeuvre for the Bank of Japan, even if the central bank did make policy interest rates negative in 2016 and conducted ever more radical asset buying such that the central bank owns Japanese government bonds worth a little more than Japan’s GDP.[13] Such squeezed macro weapons seemed to offer little against the general drop in demand from an ageing, then declining, population that peaked at 128 million in 2008.[14]

Micro reforms were always politically difficult. Abe, nonetheless, succeeded in driving up the labour participation rate. The employment rate of the working-age population rose from 70% in 2012 to 78% in 2020[15] helped by a jump in the female labour-force participation rate from 69% to 79% over that time – even if many of these people were ‘freeters’, the Japanese word for casuals or freelancers.[16] Abe pushed measures to increase the birth rate from about 1.5 children per female that is below the replacement rate of 2.1.[17] He won public support for immigration such that a record 2.2 million foreigners lived in Japan in 2019, 1.8% of the country’s now-population of 126 million.[18] Abe helped drive trade deals such as one with the EU and an Asia-Pacific one minus China and the US. He oversaw an improvement in corporate governance. Mixed in that were calls for the private sector to boost wages to bolster consumption.

But Abe never eradicated onerous regulation on business. Nor did he mimic the money printing of Takahashi, an ex-governor of the Bank of Japan (1911-13), a former prime minister (1921-22) and finance minister for the fourth time from 1931 to 1936 (when soldiers assassinated him after, judging the economy healthy enough, he reduced military spending). Governments print money via fiscal policy when they hand money to the public, even if the mechanism involves the central bank acting as the government’s banker not as an ‘independent’ body that targets low inflation. Governments typically print money when rather than sell bonds to fund a deficit they get their central bank to instead buy the bonds at auction. Many would argue that a government is printing money when its central bank is buying enough bonds in the secondary market under a quantitative-easing program to cover the government’s deficit.

The risk with money printing is that inflation could roar out of control if too much money is handed to the public. But under Takahashi inflation stayed tame. And thanks to such episodes, in many advanced countries with low inflation and languid economies, money printing is gaining adherents, often under the guise of ‘Modern Monetary Theory’.

Perhaps Japan under Suga will chose this option. Or maybe Suga will pursue more aggressive quantitative easing. Or possibly Suga will help policymakers walk back from a policy of inflation at any cost or postpone when a 2% inflation target must be hit, and he will only pursue micro reforms.[19] One more certain outcome is that whatever Suga does with the ailing Japanese economy will hold lessons for the world.

By Michael Collins, Investment Specialist

Central bank asset holdings as a percentage of GDP

Source: Federal Reserve of the Bank of St Louis

research.stlouisfed.org/publications/economic-synopses/2019/07/15/the-asset-holdings-of-the-bank-of-japan

[1] Abe is the grandson of prime minister Nobusuke Kishi (1957-1960), who was one of the architects of Japan post-World War II. He is the grand-nephew of prime minister Eisaku Satō (1964-1972).

[2] Ben Bernanke, former chairman of the Federal Reserve. “Some thoughts on monetary policy in Japan.” Speech to the Japan Society of Monetary Economics, Tokyo, Japan, 31 May 2003. federalreserve.gov/boarddocs/speeches/2003/20030531/

[3] IMF. World Economic Outlook database. October 2019. General government structural balance. imf.org/external/pubs/ft/weo/2019/02/weodata/index.aspx

[4] Japan’s general government structural balance was reduced from 7.6% of GDP in 2012 to an average 3.1% of GDP from 2017 to 2019. IMF op cit.

[5] Japan’s economy shrank a record 28% annualised pace in the second quarter

[6] IMF. Op cit. The inflation rate is from the average rate for each year.

[7] OECD. GDP per hour worked. data.oecd.org/lprdty/gdp-per-hour-worked.htm

[8] Federal Reserve Bank of St Louis. ‘The asset holdings of the Bank of Japan.’ 15 July 2019. research.stlouisfed.org/publications/economic-synopses/2019/07/15/the-asset-holdings-of-the-bank-of-japan

[9] Bloomberg News. ‘Suga sets sights on structural reforms for debt-ridden Japan.’ 15 September 2020. bloomberg.com/news/articles/2020-09-15/suga-sets-sights-on-structural-reforms-for-debt-ridden-japan

[10] Simon Winchester. ‘Pacific. The ocean of the future.’ William Collins. Paperback edition 2016. Chapter 2. Mr Ibuka’s radio revolution. Pages 83 to 119.

[11] RIMES

[12] IMF. Op cit.’General government’ net and gross debt.

[13] Federal Reserve Bank of St Louis. ‘The asset holdings of the Bank of Japan.’ Op cit.

[14] The World Bank. ‘Population dashboard.’ datatopics.worldbank.org/health/population

[15] Federal Reserve Bank of St Louis. ‘Employment rate: Aged 15-64: All persons for Japan.’ fred.stlouisfed.org/series/LREM64TTJPQ156N

[16] Federal Reserve Bank of St Louis. ‘Employment rate: Aged 25-54: Females for Japan.’ fred.stlouisfed.org/series/LREM25FEJPM156S

[17] OECD. ‘Family database. ‘SF2.1: Family fertility rates.’ 3 June 2019. oecd.org/social/family/SF_2_1_Fertility_rates.pdf

[18] Nikkei Asian Review. ‘Japan immigration hits record high as foreign talent fills gaps.’ 13 April 2019. asia.nikkei.com/Spotlight/Japan-immigration/Japan-immigration-hits-record-high-as-foreign-talent-fills-gaps

[19] Bloomberg News. ‘Suga to help the Bank of Japan tiptoe away from inflation at any cost.’ 18 September 2020. bloomberg.com/news/articles/2020-09-17/suga-to-help-boj-tiptoe-away-from-inflation-at-any-cost?sref=ORbm2mFs

Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 (‘Magellan’) and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.